Early in 2020, as the world was entering the first stage of what was to become ongoing lockdowns, images were broadcast around the world showing pollution free skies and clearing waterways. If there was any doubt before, here was pictorial evidence that our modern way of life was having an undeniable impact on the world around us.

For those of us who manage property, whether it be commercial office, retail or industrial, it called into question the steps that are being taken to minimize the footprint that these assets leave behind. Whilst the lockdowns gave a temporary reprieve, clearly a sustainable solution is called for that balances economic reality with environmental concerns. We want vibrant CBDs and places where people can gather to share ideas and communicate about their work.

We need new developments and exciting architecture and cutting edge technology. We also want to leave a healthy, safe and vibrant planet for the next generation. It is incumbent on building managers to make sure we are not making the problem worse. When it is in our control to find the solution.

It doesn’t matter what your title is, if you have a role to play in the management of a commercial asset, you have a role to play in reducing their emissions.

And whether or not you work for a company that has a reporting obligation, it is worth knowing the categories of emissions deemed reportable, and thinking about how to reduce them at every level.

Environment, Social and Governance (ESG)

The recently elected Labor Government has set a target of reducing emissions by 43% by 2030, from a baseline of 2005, maintaining their goal of Net Zero by 2050 in line with the Paris Agreement. There is widespread support for the Net Zero commitment and the reduction of carbon emissions as a means to avoid breaching the 1.5oC global warming threshold. However there is no denying that the 2050 target, together with the myriad of disclosure requirements and reporting obligations, puts pressure on businesses to optimize their ESG performance whilst simultaneously delivering strong returns for their shareholders.

Currently the more onerous mandatory reporting obligations are focused on the largest emitters in the country, but with increasing pressure from major investors for companies to move towards global reporting standards, the ESG requirements on all companies are likely to grow.

NGER

In Australia, the Clean Energy Regulator is a Federal Government body whose role it is to oversee emissions reporting by registered corporations under the National Greenhouse and Energy Reporting (NGER) framework. Registered corporations (ie corporations that meet the threshold) have the following obligation: To report all greenhouse gas emissions, energy production and energy consumption from facilities under the operational control of the registered controlling corporation or members of its group. The greenhouse gases that are reported under the NGER Scheme include:

- carbon dioxide (CO2)

- methane (CH4)

- nitrous oxide N2O)

- sulphur hexafluoride (SF6)

- specified kinds of hydro fluorocarbons and perfluorocarbons”

This includes the categorisation and monitoring of Scope 1, 2 and 3 carbon emissions.

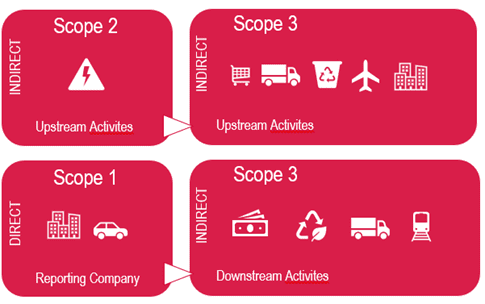

What is Scope 1, 2 & 3 emissions?

Scope 1, 2 and 3 emissions are the categories given to carbon emissions by the Greenhouse Gas (GHG) Protocol and against which they need to be reported under the NGER. The GHG Protocol developed from a partnership between the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD). According to their website, the GHG Protocol 1:

supplies the world’s most widely used greenhouse gas accounting standards. The Corporate Accounting and Reporting Standard provides the accounting platform for virtually every corporate GHG reporting program in the world.

Scope 1 emissions – direct emissions

These emissions are released into the atmosphere as a direct result of an activity by a facility, owned or controlled by the reporting company.

For example:

- production of electricity from burning coal;

- the combustion of fuel in fleet vehicles;

- the combustion of fuels in stationary sources like boilers, furnaces and incinerators;

- fugitive emissions, which is the unintentional leaking of gases or vapours from pressurised containers such as valves, pumps, storage tanks and compressors; and

- manufacturing or processing of materials and chemicals like cement manufacturing, aluminium smelting and petrochemical processing.

Scope 2 emissions – indirect emissions under our control

These are emissions released into the atmosphere from the indirect consumption of an energy commodity. For example the use of purchased electricity where that electricity is generated by burning coal at another facility.

Scope 3 emissions – indirect emissions from third party sources

These emissions are indirect greenhouse gas emissions generated in the wider community. They are outside the direct control of the reporting entity and are not required to be reported under NGER. Examples of these emissions are:

- employee business travel in transport not owned by the company (like flying on a commercial airline)

- employees commuting to and from work

- transportation of purchased fuels; and

- transport and disposal of waste

What emissions do buildings produce?

Scope 1 and 2 emissions are those which are owned or controlled by the company. If there is plant on site such as a boiler unit, or there is faulty equipment which is unintentionally leaking gases or vapours, then Scope 1 emissions are produced. For a typical commercial office tower or retail centre it is more probable the emissions fall under Scope 2, with the main emission being the consumption of electricity. Scope 3 emissions are ostensibly outside of our control, but if you look at the bigger picture, and take into account the value chain, then we have a lot more command than we realise.

If we consider activities such as people movement, waste minimisation, travel, the consumption of goods and services, and the treatment of fitout and plant at the end of its useful life, there is still much to be done in this space. Whilst not yet required in Australia, mandatory reporting on Scope 3 emissions is being introduced in other countries. Not only would it be prudent for us to start thinking about how we quantify these emissions from a reporting standpoint, it may just make the difference in our net zero target.

If you wish to know more about our service offering please email admin@reddzebra.com or contact one of our offices.

Special thanks to our copy writer Christine O’Hara cohara@cohesivecopy.com.au

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}