The commercial property sector is at a crossroads. For years, we’ve been operating on assumptions that no longer match reality — assumptions about occupancy, asset value, tenant behaviour, building condition, and investment horizons. But the biggest unspoken truth is this: hybrid work has already reshaped asset value, and most of the industry is still pretending it hasn’t happened.

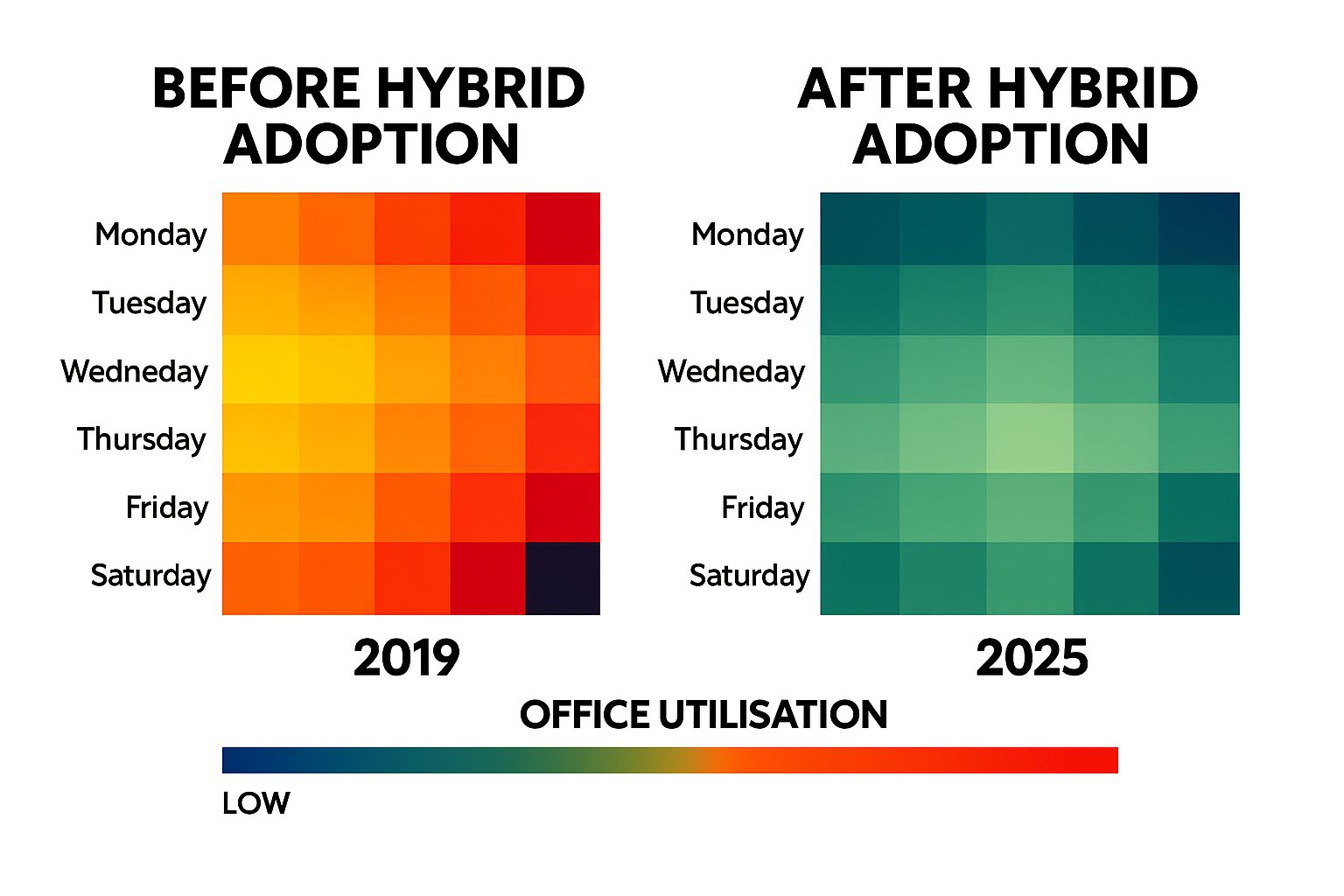

1. Utilisation Data Doesn’t Lie — Occupancy Assumptions Do

Hybrid work has structurally reshaped space demand. Redd Zebra highlights this in its article “A Guide to Asset Lifecycle Management”, noting the “ongoing debate over work‑from‑home and hybrid working models, which threaten corporations’ demand” for traditional office environments. CBRE’s 2024 APAC Office Occupier Survey reinforces the trend, showing office attendance has stabilised at new hybrid norms, with more than 60% of companies reaching a steady state of hybrid utilisation. Yet, valuations and forecasts often cling to pre 2020 utilisation assumptions.

The uncomfortable truth?

- Many CBD assets are still valued on the basis of occupancy patterns that no longer exist.

- This disconnect creates a valuation bubble built on optimism rather than evidence.

Suggested image:

2. The Industry’s Short-Termism Is Fueling a Long-Term Problem

The commercial property industry has long been criticised for focusing too heavily on 3–5 year return horizons. Redd Zebra has been explicit about this in “Commercial Property Investment Too Focused on Short Term Returns”, exposing the long term structural risk. CBRE’s Asia Pacific Real Estate Market Outlook 2025 forecasts widening performance divergence between prime and non‑core assets — a clear indicator of rising obsolescence and mispriced risk.

When short term yield takes priority:

- Essential lifecycle investment is delayed

- Buildings age faster

- Obsolescence accelerates

- Future repositioning costs balloon

Short-term thinking leads to long-term fragility.

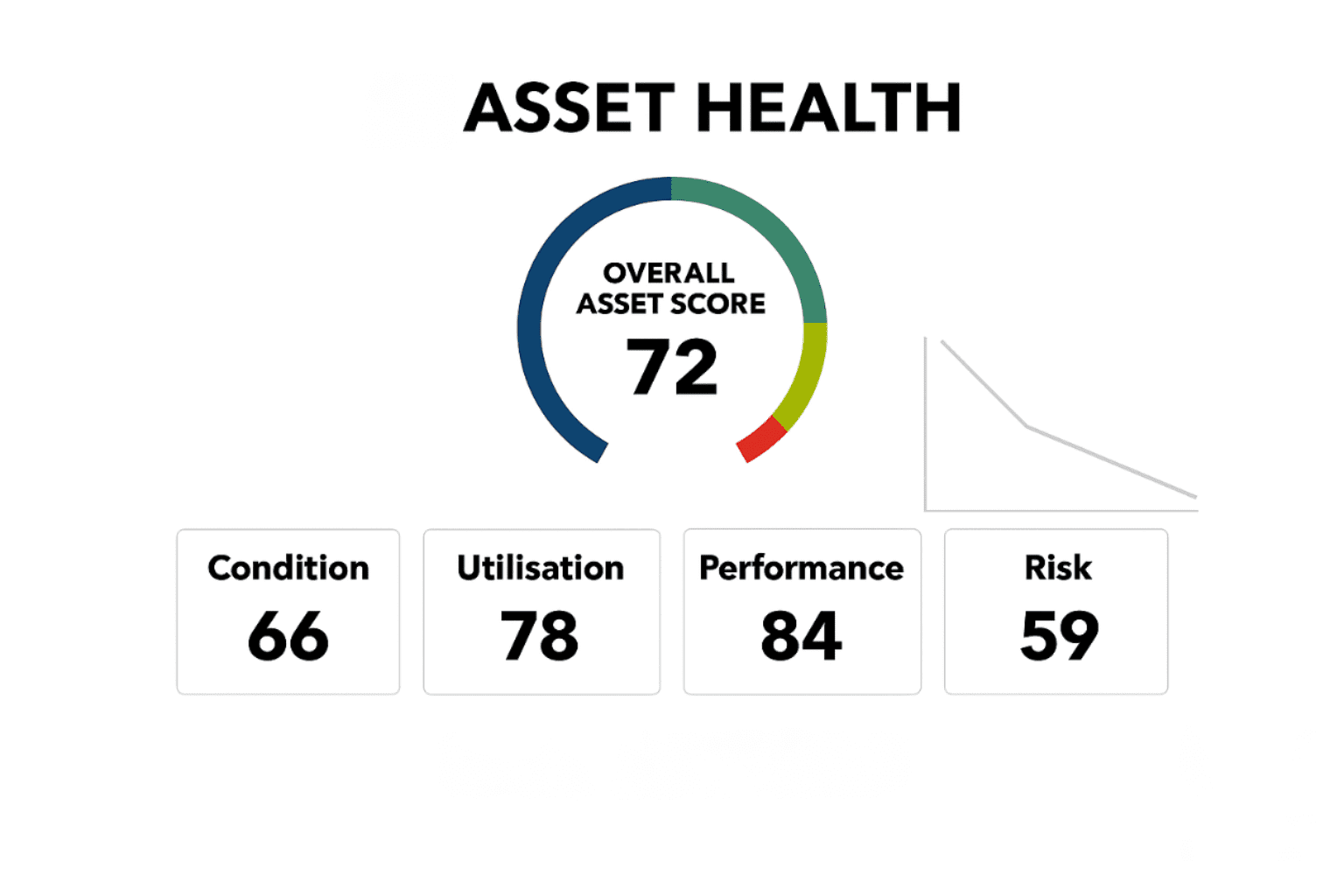

3. AI Is Quietly Exposing the Truth Behind the Numbers

AI is rapidly reshaping Australia’s commercial property landscape, bringing precision, transparency, and data driven insights to decision-making. Redd Zebra’s article “AI in Australia’s Commercial Property Market: The Present and the Road Ahead” identifies AI’s growing role in assessing condition, forecasting lifecycle costs, and uncovering inefficiencies across portfolios. McKinsey also reports that AI could create $110B–$180B in value for real estate by uncovering operational inefficiencies and improving forecasting.

Here’s the controversial part:

AI models are revealing gaps between reported asset performance and actual performance.

These tools cut through narrative and guesswork. They expose:

- True lifecycle requirements

- Hidden risks

- Undocumented defects

- Inefficient FM processes

- Mispriced assets

AI isn’t the future. It’s the mirror — and it’s already showing us what we’ve been avoiding.

4. Tenant Leverage Has Shifted — And Landlords Know It

Tenant covenant strength and lease clarity are some of the biggest factors influencing portfolio profitability. Redd Zebra’s article “Portfolio Lease Reviews: How to Save Money” emphasises how these elements shape financial outcomes and strategic decisions. Meanwhile, JLL research shows APAC has some of the highest office attendance globally, yet tenants still demand flexibility, efficiency, and higher‑quality environments. But in a hybrid-work world, tenant leverage has fundamentally changed:

- Tenants can downsize faster

- They can negotiate harder

- They now demand flexibility as a baseline

- They know owners need to retain them more than ever

Landlords who cling to old leasing power dynamics often lose financially before they realise what happened.

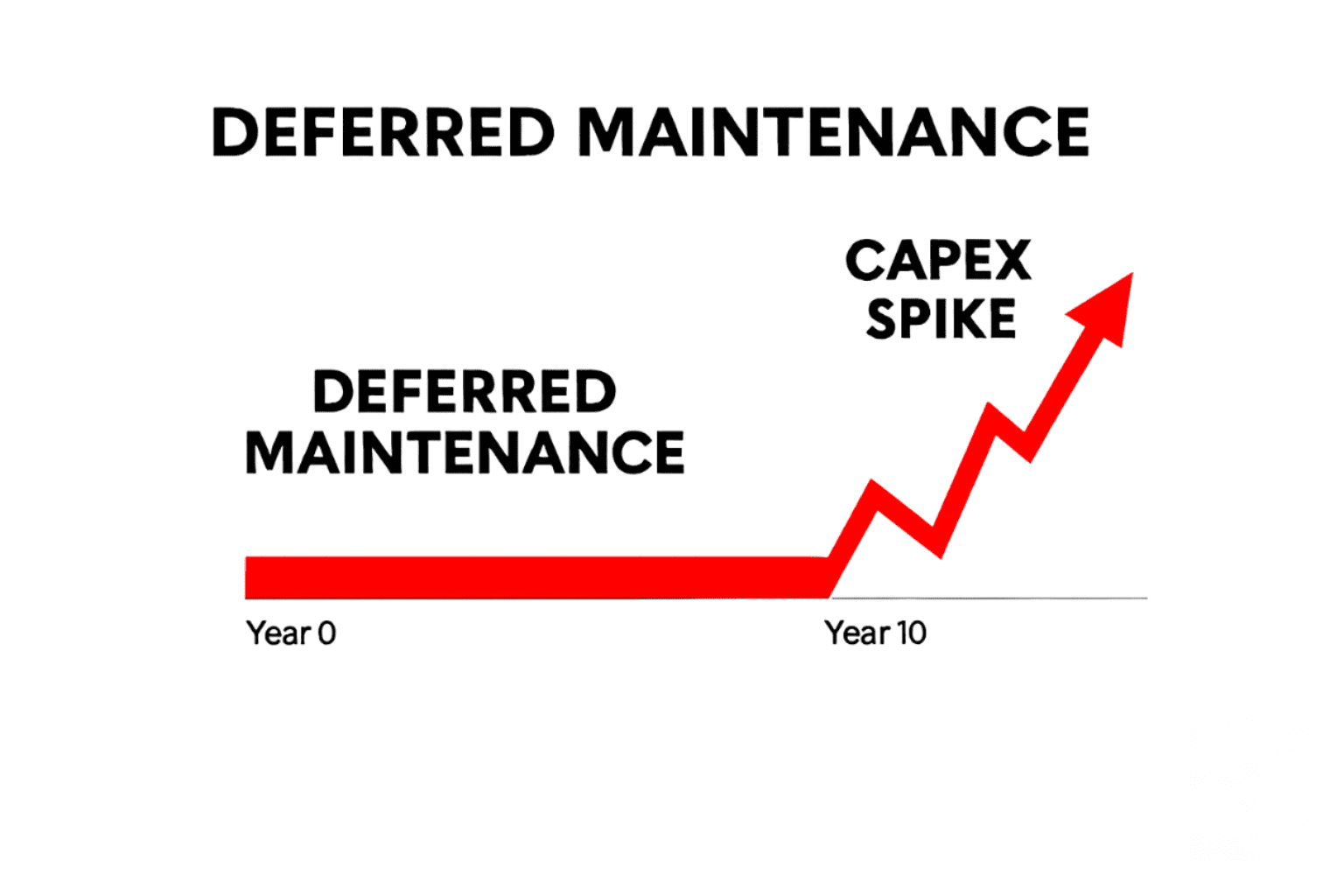

5. Obsolescence Is the Elephant in the Room

Lifecycle management and condition auditing are central to Redd Zebra’s advisory work — and for good reason. Many assets are ageing faster due to deferred investment, operational inefficiencies, or outdated design standards.

Global research reinforces the risk:

- Savills’ 2026 Global Occupier Outlook shows Grade B offices continue to face downward pressure as tenants flock to quality, ESG aligned buildings.

- RICS indicates rising obsolescence risk across secondary assets as deferred investment compounds asset deterioration.

Hybrid work compresses revenue → revenue compression reduces reinvestment → reinvestment delays accelerate obsolescence.

Here’s the hard truth:

If owners continue delaying lifecycle work because “demand will come back,” a significant portion of CBD offices will slide down the quality scale within the decade. Obsolescence isn’t theoretical — it’s measurable, predictable, and visible today.

6. The Path Forward: Think Differently, Act Differently

Redd Zebra’s philosophy is built on challenging the status quo — not for disruption’s sake, but for better outcomes. The property lifecycle requires:

- Evidence based decision-making

- Transparent asset data

- Long-term investment horizons

- Realistic utilisation modelling

- Proactive lifecycle planning

- Independent advisory free from conflicts of interest

The industry doesn’t need more optimism.

It needs clarity. Truth. Data. Strategy.

Most of all, it needs leaders willing to acknowledge that hybrid work has permanently changed the asset landscape.

Conclusion: It’s Time to Reassess What “Value” Really Means

The commercial property industry is already in a new era — even if many continue operating as though the old one still exists.

- Hybrid work has stabilised.

- Tenant expectations have evolved.

- AI has dismantled legacy assumptions.

- Obsolescence is accelerating.

The longer organisations delay confronting this reality, the steeper the eventual adjustment becomes.

Redd Zebra helps property owners, investors, lenders, and occupiers understand their true asset position — and what decisions will shape the next decade of value creation. For more information about how Redd Zebra can help, contact us on admin@reddzebra.com or visit our website at www.reddzebra.com.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}